From 8 to 10 April 2026, the Centre de Recerca Matemàtica (CRM) hosted the Conference on Mathematical and Statistical Methods for Actuarial Sciences and Finance (MAF 2026). The conference is an international meeting that brings together mathematicians and statisticians to discuss new theoretical results and applications in actuarial sciences and finance.

The programme combined plenary lectures, parallel sessions organised by thematic areas, and online presentations, reflecting both the diversity of approaches and the international character of the event.

Plenary Speakers

The first plenary lecture was delivered by José Garrido (Concordia University), who presented Accounting for temporal and spatial dependencies in multi-population mortality forecasts: the “transformer” approach. His work extended transformer architectures to incorporate structural dependencies between countries, combining mortality data with exogenous variables. The proposed approach showed a significant improvement in the accuracy of long-term mortality forecasts.

|

|

On the same Wednesday, Isabel Serra (Universitat Autònoma de Barcelona) gave the talk Maximum Likelihood Approach for Risk Assessment in Finance, in which she examined financial risk assessment from the perspective of statistical inference of extreme events. Her presentation connected extreme value theory, maximum likelihood estimation, and machine learning, addressing current challenges such as temporal dependence and the presence of mixtures in the data.

|

|

On Thursday, Katrien Antonio (KU Leuven) focused her lecture on Machine Learning in an Expectation–Maximisation Framework for Nowcasting. Starting from the issue of partially observable information and reporting delays, she proposed a framework based on expectation–maximisation that integrates machine learning and deep learning techniques. Her results, particularly relevant in contexts with non-linear effects and high-dimensional data, have direct applications in the modelling of claims related to weather-related events.

|

|

That same day, Claude Lefèvre (Université Libre de Bruxelles) addressed Insurance Coverage for SIR Epidemic Models, centred on stochastic SIR-type models for epidemics. From an actuarial perspective, he analysed premium determination using the equivalence principle, paying particular attention to the total duration of the epidemic process and the expected number of cases. His talk highlighted the mathematical complexity that arises when translating epidemiological models into insurance products.

|

|

On Friday, Pietro Millossovich (Bayes Business School) presented Three Actuarial Applications of an Iterative Least Square Monte Carlo Algorithm. His lecture demonstrated the flexibility of the Least Squares Monte Carlo (LSMC) method for solving complex problems in life insurance and mortality modelling. Through three applications, he illustrated how this approach allows optimal stopping problems to be addressed while significantly reducing computational complexity.

|

|

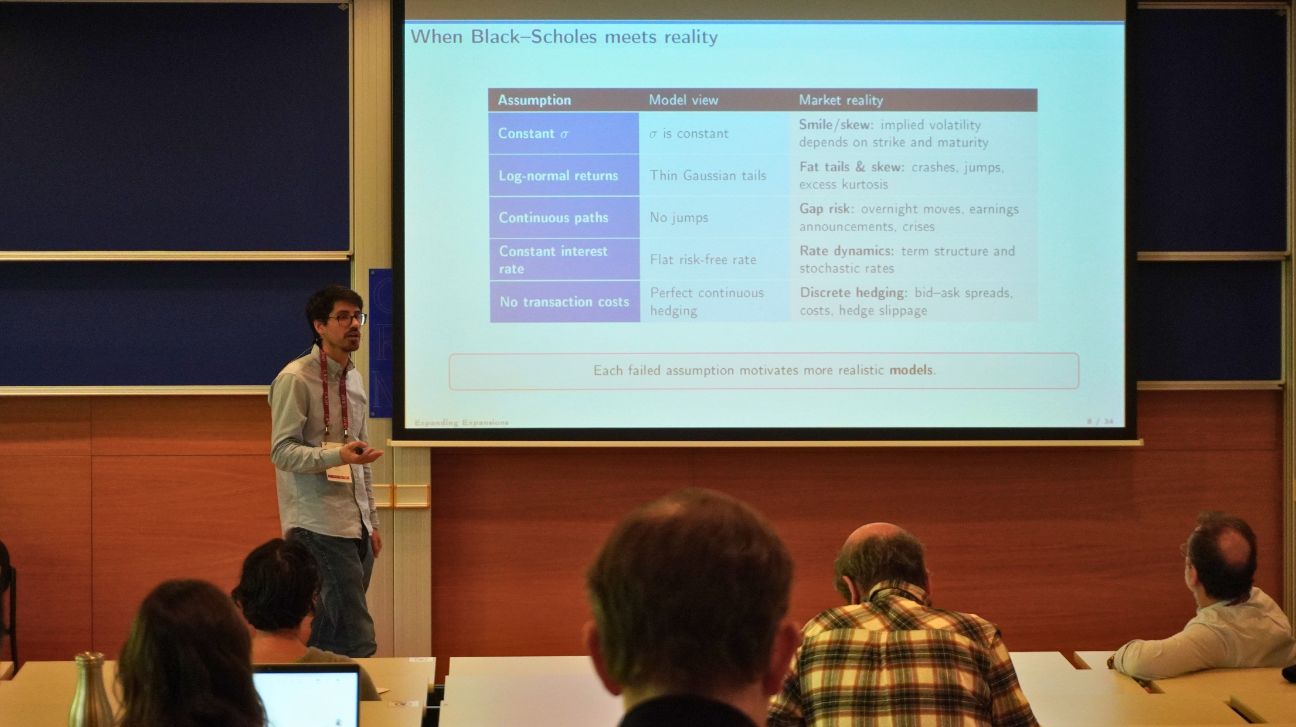

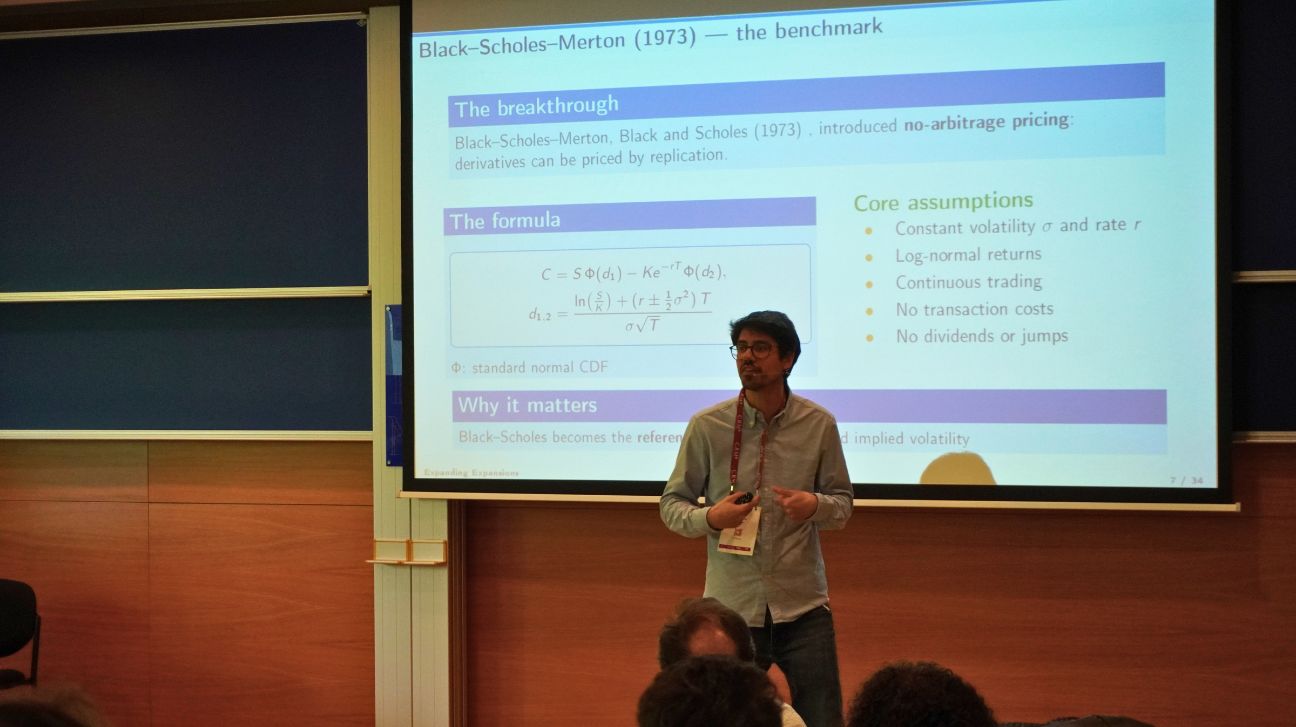

To conclude, Raúl Merino (VidaCaixa), in Expanding Expansions: Beyond Vanillas, reviewed classical expansion methods in quantitative finance and showed how they can be applied beyond so-called vanilla products, i.e. standard financial instruments with simple structures such as basic options or bonds. His talk focused especially on interest rate markets and, using Malliavin calculus techniques, presented approximations capable of systematically capturing convexity effects.

|

|

Parallel Sessions and Thematic Areas

In addition to the plenary lectures, MAF 2026 was structured around parallel and online sessions organised into eight major thematic areas, reflecting the main current research directions in actuarial sciences and finance:

- Climate Risks and Sustainable Finance (ESG), focused on climate risks, energy transition, natural disasters, and sustainable finance.

- Longevity, Health, and Pension Systems, devoted to population ageing, mortality, and the design of sustainable pension systems.

- Machine Learning and Artificial Intelligence, featuring work on model validation, algorithmic biases, and advanced applications in finance and insurance.

- Actuarial Pricing and Count Models, focused on statistical models for pricing and reserving in non-life insurance.

- Financial Networks, Contagion, and Dependence, addressing systemic interconnections, financial contagion, and dependence modelling.

- Portfolio Management and Investment Decisions, dedicated to portfolio optimisation and risk management.

- Financial Mathematics, centred on theoretical models for the valuation of derivatives and complex financial products.

- Actuarial Mathematics, with contributions on actuarial valuation, risk, mortality, and insurance contracts.

|

|

|

|

An Interdisciplinary Meeting Space

Over the course of three days, the CRM, through MAF 2026, showcased how methodological and theoretical advances can be translated into useful tools to address some of today’s major economic and social challenges, ranging from climate change to population ageing and the digital transformation of the financial sector.

|

|

CRM CommNatalia Vallina

|

Yves Chevallard (1946–2026)

Yves Chevallard passed away on 16 March 2026. He was 79 years old. Born in Tunis, he trained at the École normale supérieure in Paris, where he earned an agrégation de mathématiques. He went on to become a professor at Aix-Marseille Université, and it was there, over...

The CRM participates in a European project studying decision-making and risk perception in mountain environments

The NeuroMunt project (POCTEFA, coordinated by the Université de Perpignan Via Domitia) studies how people make decisions under risk conditions in mountain environments, bringing together researchers from France and Spain across disciplines ranging from complex...

One Day, One Family, One Place: Poisson Geometry at CRM

On March 23rd, 2026, the Centre de Recerca Matemàtica hosted the thematic day “Poisson Geometry and Its Relatives”, a full‑day event that brought together researchers exploring Poisson geometry and several of its neighbouring areas. The programme combined classical...

Life After the PhD: Three Roads Forward

On March 18, the BGSMath held its first session on careers after a PhD in mathematics, bringing together three speakers with different professional trajectories and 46 early-career researchers from nine institutions.On March 18, the Barcelona Graduate School of Math...

CRM participates in the 2026 ERCOM annual meeting in Belgrade

The CRM participated in the 2026 ERCOM annual meeting in Belgrade (20–21 March), represented by Director Carme Cascante, Manager Gemma Martínez, and Scientific Activities Manager Núria Hernández. The programme focused on multidisciplinarity, mathematics and the arts,...

5 Talks, 1 Topic: A Day of Combinatorics

On March 18th, 2026, the 5 Talks in Combinatorics thematic day took place in the Joan Maragall Room at the Faculty of Philology and Communication of the University of Barcelona, in the historic building. The event focused on modern combinatorics and its connections...

Gerd Faltings Awarded the 2026 Abel Prize for Transformative Work in Arithmetic Geometry

The Norwegian Academy of Science and Letters has recognised the German mathematician for solving two of the most enduring open problems in the field.The Norwegian Academy of Science and Letters announced today that the 2026 Abel Prize goes to Gerd Faltings, director...

The Centre de Recerca Matemàtica Approves Its Strategic Plan for 2026–2030

The Centre de Recerca Matemàtica has approved its Strategic Plan for 2026 - 2030, setting priorities in research, training, and knowledge transfer. Four flagship initiatives anchor the scientific programme. The Centre de Recerca Matemàtica approved its Strategic Plan...

CRM Awards Its Prize at Exporecerca Jove for the Third Time

For the third year running, CRM visited Exporecerca Jove to award its prize to the student project with the strongest mathematical content. This edition, the jury selected two winners: Xavier Ortiz Quintana, who built a real-time 3D scanner using...

When Symmetry Breaks the Rules: From Askey–Wilson Polynomials to Functions

Researchers Tom Koornwinder (U. Amsterdam) and Marta Mazzocco (ICREA-UPC-CRM) published a paper in Indagationes Mathematicae exploring DAHA symmetries. Their work shows that these symmetries shift Askey–Wilson polynomials into a continuous functional setting,and...

Homotopy Theory Conference Brings Together Diverse Research Perspectives

The Centre de Recerca Matemàtica hosted 75 mathematicians from over 20 countries for the Homotopy Structures in Barcelona conference, held February 9-13, 2026. Fourteen invited speakers presented research spanning rational equivariant cohomology theories, isovariant...

Three ICM speakers headline the first CRM Faculty Colloquium

On 19 February 2026, the Centre de Recerca Matemàtica inaugurated its first CRM Faculty Colloquium, a new quarterly event designed to bring together the mathematical community around the research carried out by scientists affiliated with the Centre. The CRM auditorium...