From 8 to 10 April 2026, the Centre de Recerca Matemàtica (CRM) hosted the Conference on Mathematical and Statistical Methods for Actuarial Sciences and Finance (MAF 2026). The conference is an international meeting that brings together mathematicians and statisticians to discuss new theoretical results and applications in actuarial sciences and finance.

The programme combined plenary lectures, parallel sessions organised by thematic areas, and online presentations, reflecting both the diversity of approaches and the international character of the event.

Plenary Speakers

The first plenary lecture was delivered by José Garrido (Concordia University), who presented Accounting for temporal and spatial dependencies in multi-population mortality forecasts: the “transformer” approach. His work extended transformer architectures to incorporate structural dependencies between countries, combining mortality data with exogenous variables. The proposed approach showed a significant improvement in the accuracy of long-term mortality forecasts.

|

|

On the same Wednesday, Isabel Serra (Universitat Autònoma de Barcelona) gave the talk Maximum Likelihood Approach for Risk Assessment in Finance, in which she examined financial risk assessment from the perspective of statistical inference of extreme events. Her presentation connected extreme value theory, maximum likelihood estimation, and machine learning, addressing current challenges such as temporal dependence and the presence of mixtures in the data.

|

|

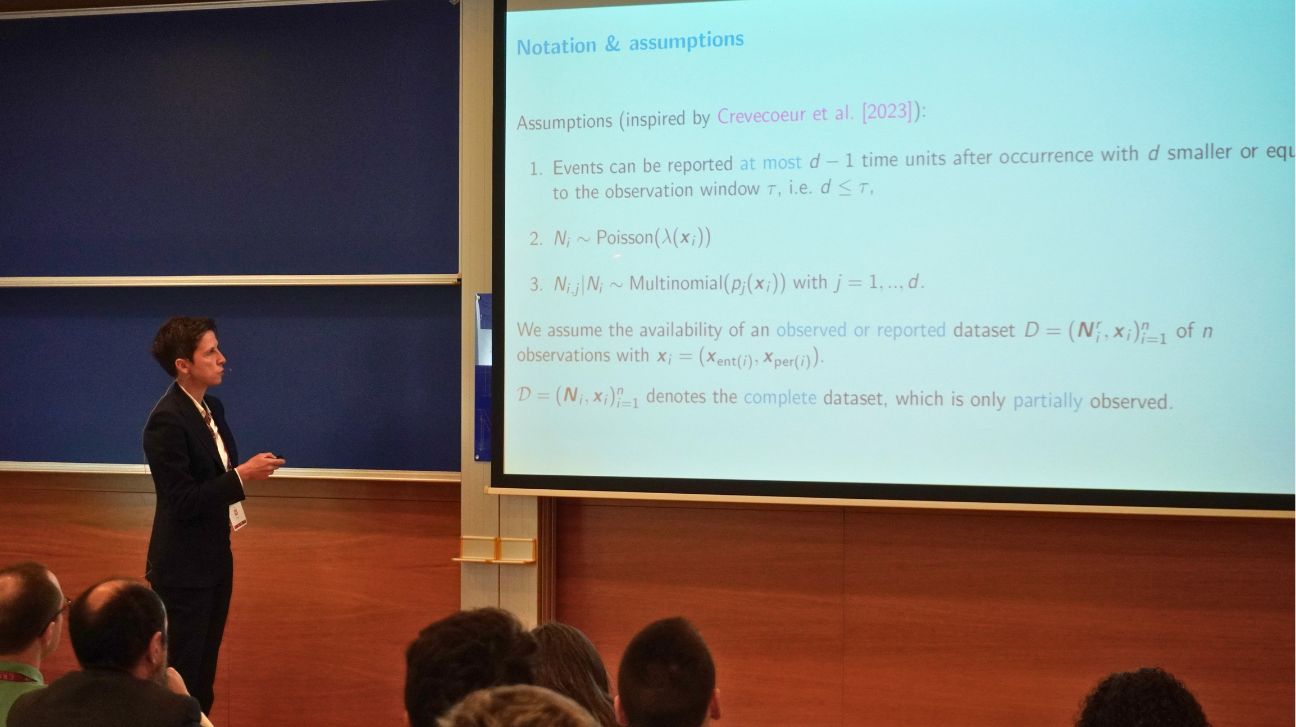

On Thursday, Katrien Antonio (KU Leuven) focused her lecture on Machine Learning in an Expectation–Maximisation Framework for Nowcasting. Starting from the issue of partially observable information and reporting delays, she proposed a framework based on expectation–maximisation that integrates machine learning and deep learning techniques. Her results, particularly relevant in contexts with non-linear effects and high-dimensional data, have direct applications in the modelling of claims related to weather-related events.

|

|

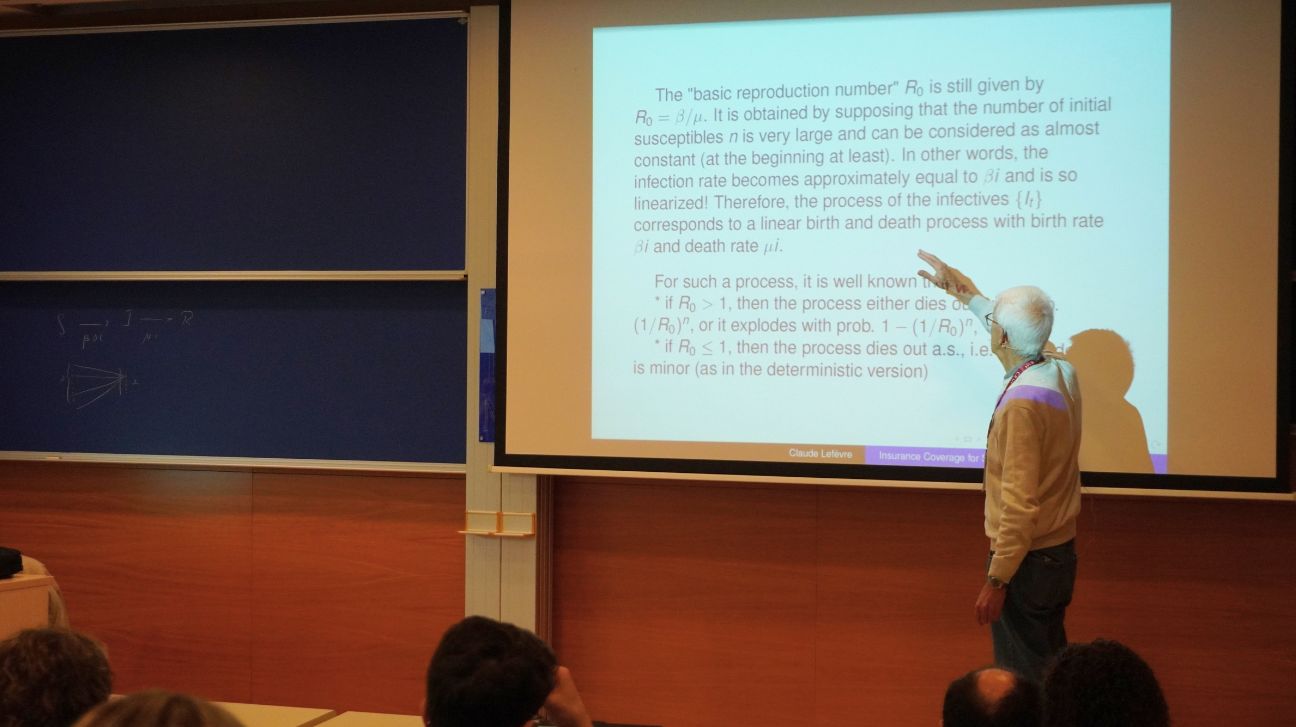

That same day, Claude Lefèvre (Université Libre de Bruxelles) addressed Insurance Coverage for SIR Epidemic Models, centred on stochastic SIR-type models for epidemics. From an actuarial perspective, he analysed premium determination using the equivalence principle, paying particular attention to the total duration of the epidemic process and the expected number of cases. His talk highlighted the mathematical complexity that arises when translating epidemiological models into insurance products.

|

|

On Friday, Pietro Millossovich (Bayes Business School) presented Three Actuarial Applications of an Iterative Least Square Monte Carlo Algorithm. His lecture demonstrated the flexibility of the Least Squares Monte Carlo (LSMC) method for solving complex problems in life insurance and mortality modelling. Through three applications, he illustrated how this approach allows optimal stopping problems to be addressed while significantly reducing computational complexity.

|

|

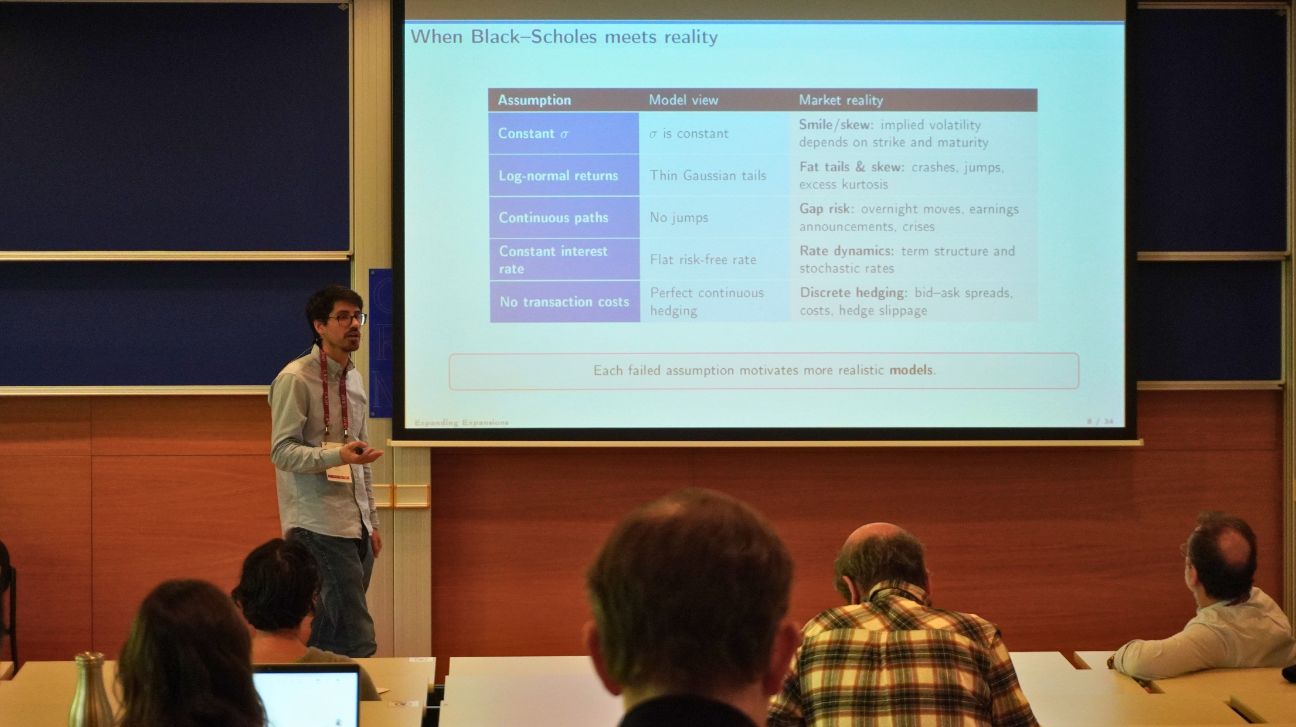

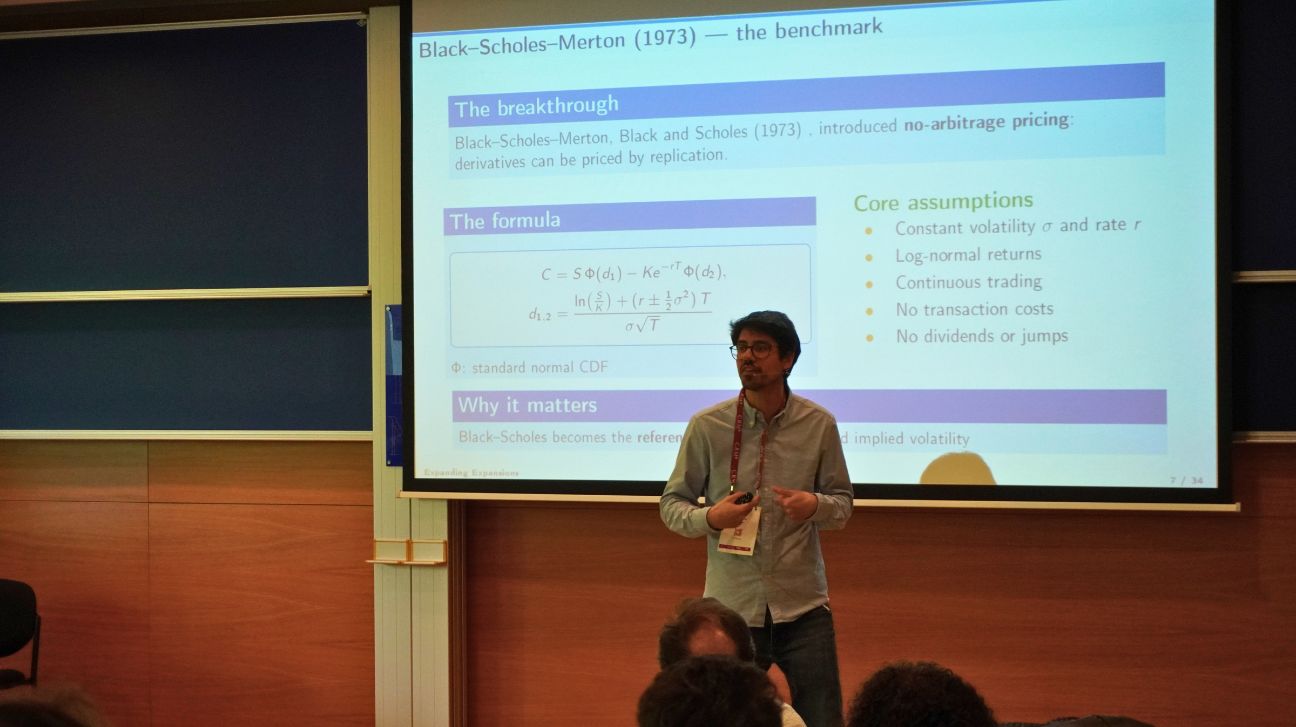

To conclude, Raúl Merino (VidaCaixa), in Expanding Expansions: Beyond Vanillas, reviewed classical expansion methods in quantitative finance and showed how they can be applied beyond so-called vanilla products, i.e. standard financial instruments with simple structures such as basic options or bonds. His talk focused especially on interest rate markets and, using Malliavin calculus techniques, presented approximations capable of systematically capturing convexity effects.

|

|

Parallel Sessions and Thematic Areas

In addition to the plenary lectures, MAF 2026 was structured around parallel and online sessions organised into eight major thematic areas, reflecting the main current research directions in actuarial sciences and finance:

- Climate Risks and Sustainable Finance (ESG), focused on climate risks, energy transition, natural disasters, and sustainable finance.

- Longevity, Health, and Pension Systems, devoted to population ageing, mortality, and the design of sustainable pension systems.

- Machine Learning and Artificial Intelligence, featuring work on model validation, algorithmic biases, and advanced applications in finance and insurance.

- Actuarial Pricing and Count Models, focused on statistical models for pricing and reserving in non-life insurance.

- Financial Networks, Contagion, and Dependence, addressing systemic interconnections, financial contagion, and dependence modelling.

- Portfolio Management and Investment Decisions, dedicated to portfolio optimisation and risk management.

- Financial Mathematics, centred on theoretical models for the valuation of derivatives and complex financial products.

- Actuarial Mathematics, with contributions on actuarial valuation, risk, mortality, and insurance contracts.

|

|

|

|

An Interdisciplinary Meeting Space

Over the course of three days, the CRM, through MAF 2026, showcased how methodological and theoretical advances can be translated into useful tools to address some of today’s major economic and social challenges, ranging from climate change to population ageing and the digital transformation of the financial sector.

|

|

CRM CommNatalia Vallina

|

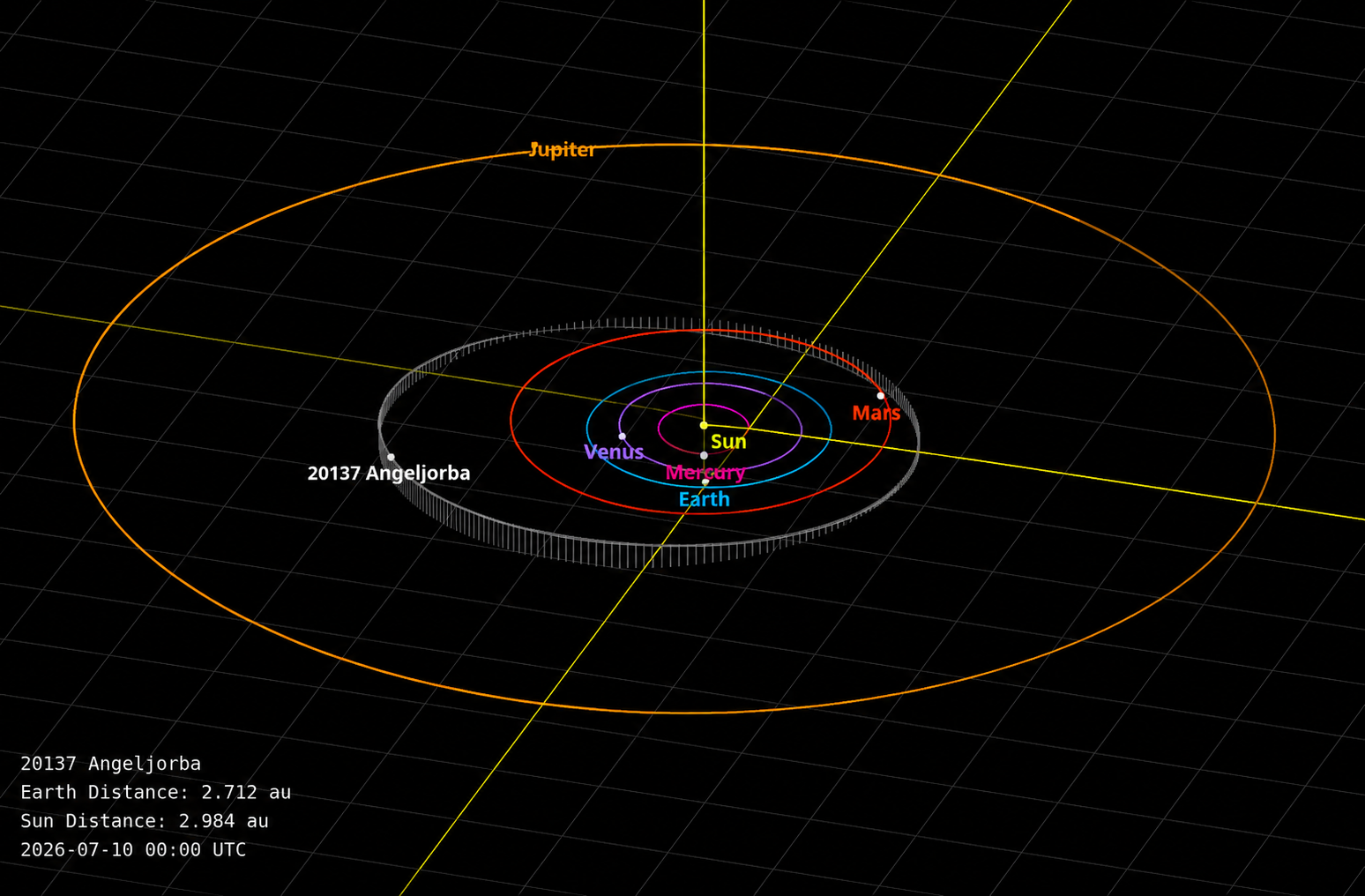

An asteroid now carries the name of Àngel Jorba

An asteroid has been named (20137) Àngeljorba in honour of Àngel Jorba (1963-2025), UB professor and CRM affiliated researcher. Approved by the IAU, the name recognises his career in dynamical systems and celestial mechanics, from the orbital theory behind ESA's SOHO...

BIMR 2026: a first taste of research for future mathematicians

For four weeks in July 2026, the Centre de Recerca Matemàtica hosted the Barcelona Introduction to Mathematical Research (BIMR), a BGSMath summer programme built to give undergraduate and master's students a first, genuine experience of mathematical research and a...

Cambridge University Press publishes Single and Multiple Number Series, co-authored by Sergey Tikhonov (ICREA, CRM)

Sergey Tikhonov (ICREA, CRM) is one of four authors of the volume, published in the Encyclopedia of Mathematics and Its Applications series, which develops the theory of number series in one and several dimensions.Cambridge University Press has...

The 22nd JISD brings dynamical systems and PDEs to the CRM

The 22nd School on Interactions between Dynamical Systems and Partial Differential Equations (JISD) is taking place at the Centre de Recerca Matemàtica from 29 June to 3 July 2026. Four advanced courses and a poster session gather researchers in dynamical systems and...

CRM Annual Report 2025: A Year in Mathematics

CRM June Newsletter

ENHANCE Poster Earns Honorable Mention at FEniCS 2026 in Paris

Harmonic Analysis and PDEs Summer School at the CRM

Four mini-courses, from incompressible fluids to the geometry of boundaries, around a shared body of technique. CRM Auditorium, 15 to 18 June 2026.A rotating blob of fluid that never settles into rest. The ragged edge of a region in the plane. A weighted inequality...

An extension to higher dimensions of Carleson’s ε² conjecture

A recent article by Ian Fleschler (Princeton University), Xavier Tolsa (UAB – ICREA – CRM) and Michele Villa (Ikerbasque and UPV/EHU), published in Inventiones Mathematicae, establishes a higher-dimensional version of the well-known ε² conjecture of Carleson, a...

Hypatia 2026: Modelling Life, Sharing Ideas

From June 8 to 11, 2026, the Centre de Recerca Matemàtica (CRM) hosted a new edition of the Hypatia Graduate Summer School, a space for advanced training and scientific exchange for young researchers in mathematics and its applications. This year’s school revolved...

Eva Miranda and Xavier Tolsa elected to the Royal Academy of Sciences

Spain's Royal Academy of Sciences has elected two mathematicians from the CRM community to its Mathematics section within the space of a month.The plenary of Spain’s Royal Academy of Exact, Physical and Natural Sciences has elected Eva Miranda (UPC, CRM) a...