The 5th edition of the Barcelona Summer School on Stochastic Analysis and Quantitative Finance took place from July 21 to 25, 2025, at the Centre de Recerca Matemàtica (CRM), marking the revival of an academic tradition interrupted by the pandemic. The program offered advanced training in cutting-edge topics such as rough volatility, path signatures, and weather derivatives, featuring international experts and a strong presence of early-career researchers.

The 5th Barcelona Summer School on Stochastic Analysis and Quantitative Finance marked an important milestone in the revival of a valued academic tradition. After a hiatus caused by the pandemic, this edition sought to re-establish the series of summer schools previously held at the Centre de Recerca Matemàtica (CRM) between 2012 and 2018. Its main objective was to provide advanced training in cutting-edge topics in stochastic analysis and quantitative finance, delivered by internationally renowned experts. The school was aimed at PhD students, postdoctoral researchers, and academics, fostering both local and international collaboration while reinforcing Catalonia’s position as a leading center for mathematical research.

The academic core of the summer school consisted of three advanced courses, each offering a deep dive into a key area of contemporary research in stochastic analysis and quantitative finance. The lectures were designed not only to present theoretical developments, but also to build intuition and connect with practical applications.

- Rough Volatility by Masaaki Fukasawa (Osaka University)

Professor Fukasawa is a highly respected figure in the field of mathematical finance, known for his influential work on skewness, volatility estimation, and stochastic integration. His research has contributed significantly to the understanding of implied volatility surfaces and their asymptotic behavior, particularly in the context of rough volatility. He is also a key member of the Sekine–Fukasawa–Yano research group at Osaka University.

In his course, he emphasized intuitive understanding through simple computations and highlighted connections with classical models. Fukasawa also offered a conceptual and accessible introduction to rough volatility modeling, focusing on three key perspectives: historical volatility dynamics, the term structure of implied volatility, and market microstructure.

- An Introduction to Signatures with Applications in Finance by Christian Bayer (Weierstrass Institute)

Professor Bayer is a leading researcher in stochastic numerics and quantitative finance. His work on rough volatility, stochastic control, and the application of rough path theory to machine learning has positioned him at the forefront of modern financial mathematics.

The course introduced the theory of path signatures, a powerful tool for encoding time series data. Bayer explained how signatures can be used to encode time series and serve as approximators for functions on path space, and he explored their applications in machine learning and numerical methods for stochastic control. The course was particularly relevant for problems involving non-Markovian dynamics, such as those arising in rough volatility models.

- Weather Derivatives by Fred Espen Benth (University of Oslo)

Professor Benth is a prominent figure in the intersection of stochastic analysis, energy markets, and climate-related financial modeling. He has significantly contributed to the understanding of weather risk and its financial implications.

His course focused on weather derivatives—financial instruments linked to temperature, wind, and solar irradiation. After introducing the concept of weather risk and its role in renewable energy markets, Benth presented stochastic models suitable for describing weather dynamics, with particular emphasis on continuous-time autoregressive processes. The course also addressed pricing techniques for weather futures, including temperature-dependent pricing measures, and concluded with a discussion on hedging strategies and basis risk in standardized contracts.

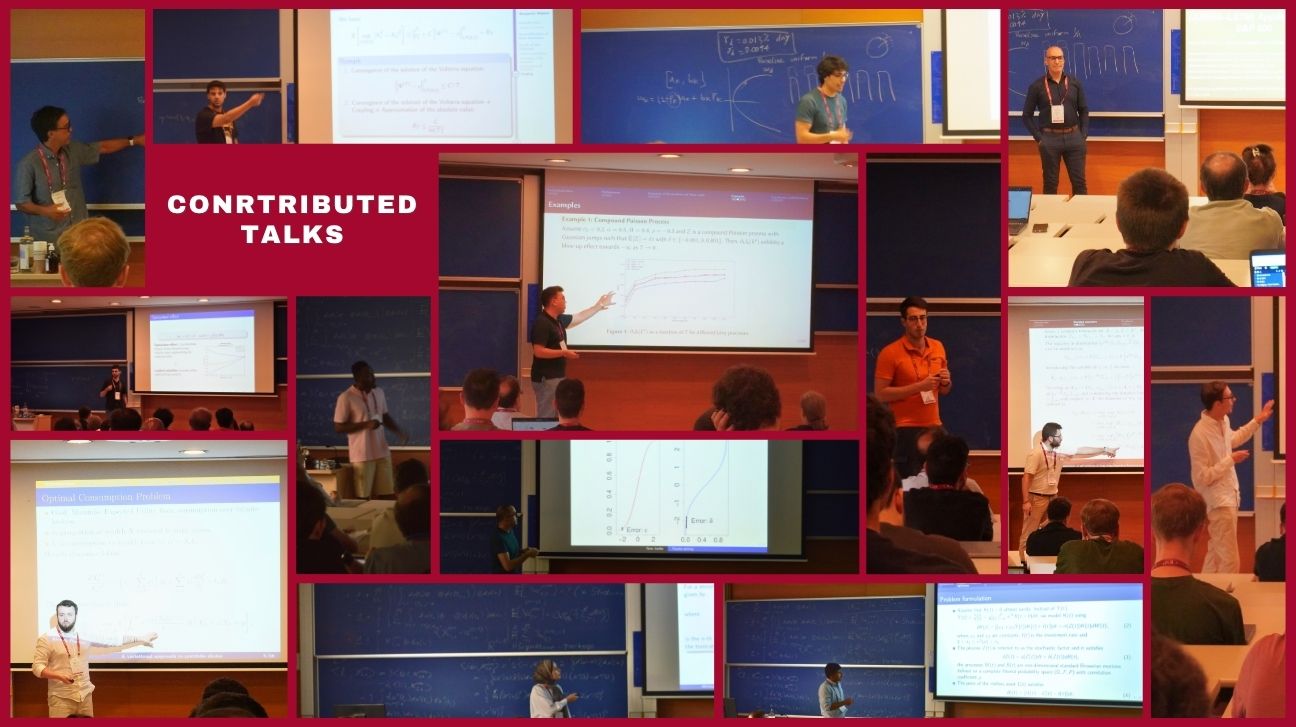

In addition to the three main courses, the summer school featured a program of contributed talks and a poster session, further enriching the academic exchange and showcasing the breadth of current research in the field. Participants from institutions across Europe and beyond presented their work on topics ranging from rough volatility and fractional processes to portfolio optimization and climate-related financial modeling. Highlights included:

- Daniele Angelini (Sapienza University of Rome) – Kolmogorov–Smirnov estimation of self-similarity in long-range dependent fractional processes

- Argimiro Arratia (Universitat Politècnica de Catalunya) – Portfolio risk and diversification strategies

- Martin Bergerhausen (University of Mannheim) – Mean-field stochastic Volterra equations: Results on the existence of weak solutions

- Òscar Burés (Universitat de Barcelona) – Short-time behavior of the At-The-Money implied volatility for the jump-diffusion stochastic volatility Bachelier model

- Mihriban Ceylan (University of Mannheim) – Global approximation theorem for signatures on the Wiener space

- Ranieri Dugo (University of Rome Tor Vergata) – Multivariate Rough Volatility

- Héctor Folgar (Universidade da Coruña and CITIC) – Pricing with rough Bergomi model in commodity markets

- Emmanuel Gnabeyeu (Sorbonne Université and Université Paris Cité) – On a Weak Stationarity Theory for FSVIEs: Finite-Time and Asymptotic Analysis, Application to Stabilized Volatility models

- Azmat Hussain (University of Central Asia) – Optimal Investment and Consumption for Assets with stochastic Volatility and Infinite Delay

- Ruben Jimenez (Universitat de Barcelona) – Fractional signature: a generalisation of the signature inspired by fractional calculus

- Gero Junike (Carl von Ossietzky Universität) – Fourier pricing techniques

- Emmet Lawless (Dublin City University) – A variational approach to portfolio choice

- Benjamin Massat (Université de Toulouse) – Quantification of limit theorem for nearly unstable Hawkes processes

- Ahmed Wafi (LMU München and Cairo University) – Hybrid econometric–ML models for return prediction under climate policy uncertainty

- Giacomo Zarfati (Sapienza Università di Roma) – Optimal Allocation With Weather Risk

The poster session enhanced the diversity of research showcased, with presentations on neural network approaches to implied volatility, Hawkes processes in energy markets, and jump-diffusion models for electricity pricing. Notable contributions included:

- Samira Amiriyan (University of Liverpool) – Neural networks and asymptotic regimes

- Konstantinos Chatziandreou (University of Amsterdam) – Execution strategies in short-term energy markets

- Christoph Gärtner (RPTU Kaiserslautern) – Shot-noise jump-diffusion models for electricity spot prices

These sessions provided an excellent platform for early-career researchers to engage with peers and senior academics, fostering collaboration and constructive feedback in a supportive environment.

The 5th edition of the Barcelona Summer School successfully rekindled a tradition of academic excellence and international collaboration. With high-level courses, dynamic discussions, and a strong sense of community, the event reaffirmed the importance of in-person scientific exchange. It also strengthened the international visibility of Catalan research in mathematics, setting a promising precedent for future events. The CRM looks forward to building on this renewed momentum in upcoming editions.

|

|

CRM CommNatalia Vallina

|

CRM Awards Its Prize at Exporecerca Jove for the Third Time

For the third year running, CRM visited Exporecerca Jove to award its prize to the student project with the strongest mathematical content. This edition, the jury selected two winners: Xavier Ortiz Quintana, who built a real-time 3D scanner using...

When Symmetry Breaks the Rules: From Askey–Wilson Polynomials to Functions

Researchers Tom Koornwinder (U. Amsterdam) and Marta Mazzocco (ICREA-UPC-CRM) published a paper in Indagationes Mathematicae exploring DAHA symmetries. Their work shows that these symmetries shift Askey–Wilson polynomials into a continuous functional setting,and...

Homotopy Theory Conference Brings Together Diverse Research Perspectives

The Centre de Recerca Matemàtica hosted 75 mathematicians from over 20 countries for the Homotopy Structures in Barcelona conference, held February 9-13, 2026. Fourteen invited speakers presented research spanning rational equivariant cohomology theories, isovariant...

Three ICM speakers headline the first CRM Faculty Colloquium

On 19 February 2026, the Centre de Recerca Matemàtica inaugurated its first CRM Faculty Colloquium, a new quarterly event designed to bring together the mathematical community around the research carried out by scientists affiliated with the Centre. The CRM auditorium...

Trivial matemàtiques 11F-2026

Rescuing Data from the Pandemic: A Method to Correct Healthcare Shocks

When COVID-19 lockdowns disrupted healthcare in 2020, insurance companies discarded their data; claims had dropped 15%, and patterns made no sense. A new paper in Insurance: Mathematics and Economics shows how to rescue that information by...

L’exposició “Figures Visibles” s’inaugura a la FME-UPC

L'exposició "Figures Visibles", produïda pel CRM, s'ha inaugurat avui al vestíbul de la Facultat de Matemàtiques i Estadística (FME) de la UPC coincidint amb el Dia Internacional de la Nena i la Dona en la Ciència. La mostra recull la trajectòria...

Xavier Tolsa rep el Premi Ciutat de Barcelona per un resultat clau en matemàtica fonamental

L’investigador Xavier Tolsa (ICREA–UAB–CRM) ha estat guardonat amb el Premi Ciutat de Barcelona 2025 en la categoria de Ciències Fonamentals i Matemàtiques, un reconeixement que atorga l’Ajuntament de Barcelona i que enguany arriba a la seva 76a edició. L’acte de...

Axel Masó Returns to CRM as a Postdoctoral Researcher

Axel Masó returns to CRM as a postdoctoral researcher after a two-year stint at the Knowledge Transfer Unit. He joins the Mathematical Biology research group and KTU to work on the Neuromunt project, an interdisciplinary initiative that studies...

The 4th Barcelona Weekend on Operator Algebras: Open Problems, New Results, and Community

The 4th Barcelona Weekend on Operator Algebras, held at the CRM on January 30–31, 2026, brought together experts to discuss recent advances and open problems in the field.The event strengthened the exchange of ideas within the community and reinforced the CRM’s role...

From Phase Separation to Chromosome Architecture: Ander Movilla Joins CRM as Beatriu de Pinós Fellow

Ander Movilla has joined CRM as a Beatriu de Pinós postdoctoral fellow. Working with Tomás Alarcón, Movilla will develop mathematical models that capture not just the static architecture of DNA but its dynamic behaviour; how chromosome contacts shift as chemical marks...

Criteris de priorització de les sol·licituds dels ajuts Joan Oró per a la contractació de personal investigador predoctoral en formació (FI) 2026

A continuació podeu consultar la publicació dels criteris de priorització de les sol·licituds dels ajuts Joan Oró per a la contractació de personal investigador predoctoral en formació (FI 2026), dirigits a les universitats públiques i privades del...